Why Investing Beyond the U.S. Is a Risk Control Decision

As investors approach retirement, the goal of investing changes. It becomes less about predicting what will happen next and more about building a portfolio that can support real-world spending—through good markets and bad. That’s the core principle behind evidence-based investing: we focus on what we can control, and we stop pretending we can control what we can’t.

Yet one of the most common concerns we hear is this: “International investing feels riskier. I’d rather stay in the U.S.”

That concern is understandable. But from an evidence-based perspective, it reflects a focus on perceived risk, not the risks that actually matter in retirement.

What We Can’t Control

Markets don’t move in straight lines, and leadership doesn’t stay in one place forever. A disciplined investment process starts by acknowledging reality.

We cannot control:

- Which country will lead markets next year

- When market leadership will change

- Political outcomes

- Economic cycles

- Short-term market returns

- Currency movements in any given year

If those things were predictable, investing would be easy. They aren’t.

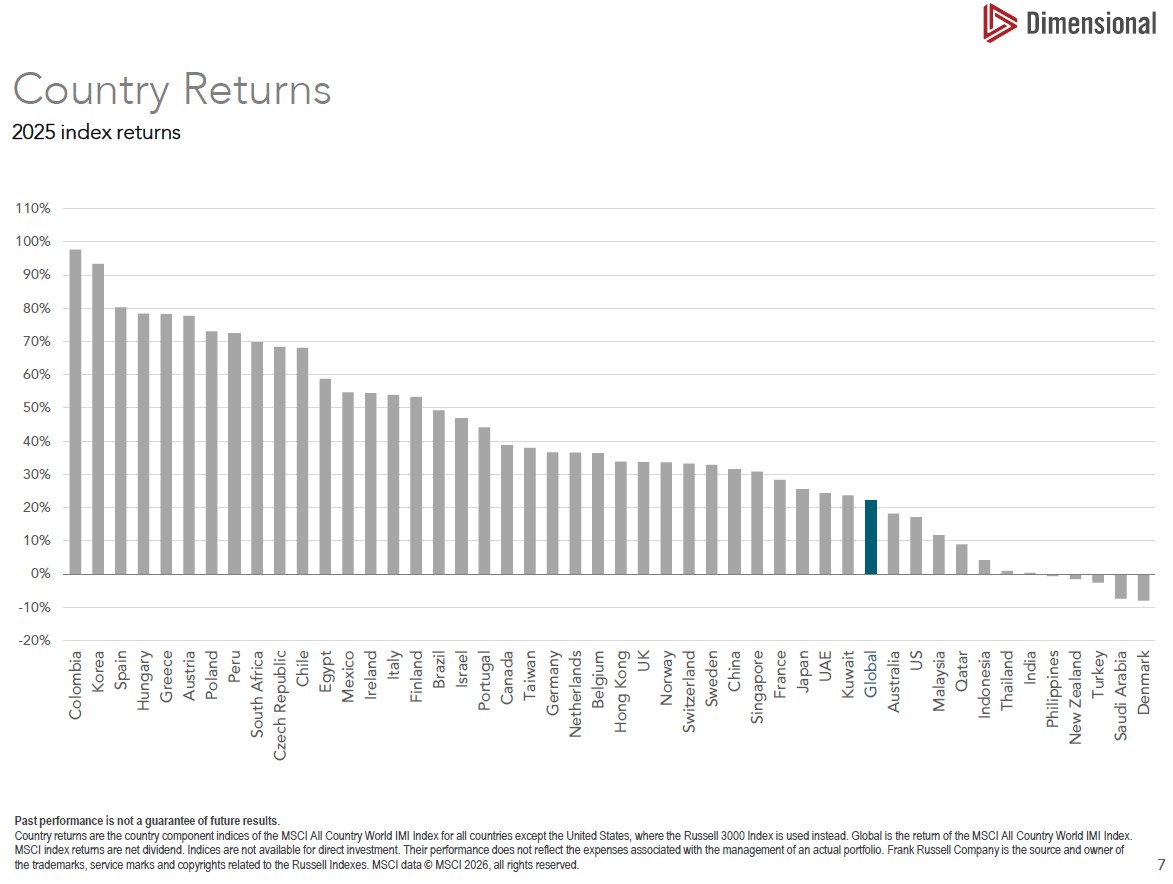

In fact, 2025 was a perfect reminder of this reality. The U.S. market had a solid year—but it was not the top performer. Several international markets outperformed, and many countries significantly outpaced the U.S.

The lesson isn’t about which country “won”.

The takeaway is that leadership rotates—and it’s unpredictable.

What We Can Control (And Why It Matters More in Retirement)

While we can’t control markets, we can control how portfolios are built and maintained.

That includes:

- Diversification

- Costs

- Asset allocation

- Rebalancing discipline

- Tax efficiency

- Withdrawal strategy

- Investor behavior

These decisions matter throughout an investor’s life. Approaching and in retirement, they matter even more.

Why We Invest Beyond the U.S.

International investing isn’t about betting on which country will outperform next. It’s about reducing reliance on any single market.

Viewed through a long-term, portfolio-construction lens, global diversification can help by:

- Spreading risk across different economic cycles

- Reducing exposure to extreme valuations in one market

- Limiting the impact of country-specific policy or economic shocks

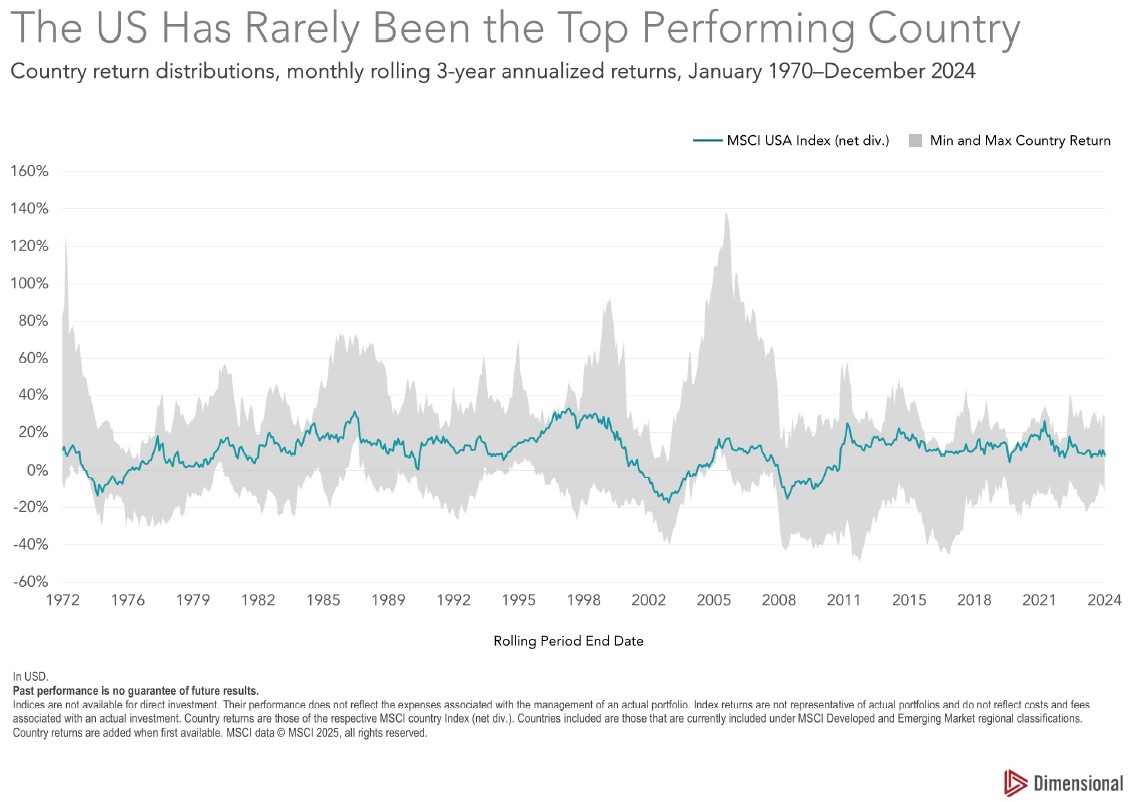

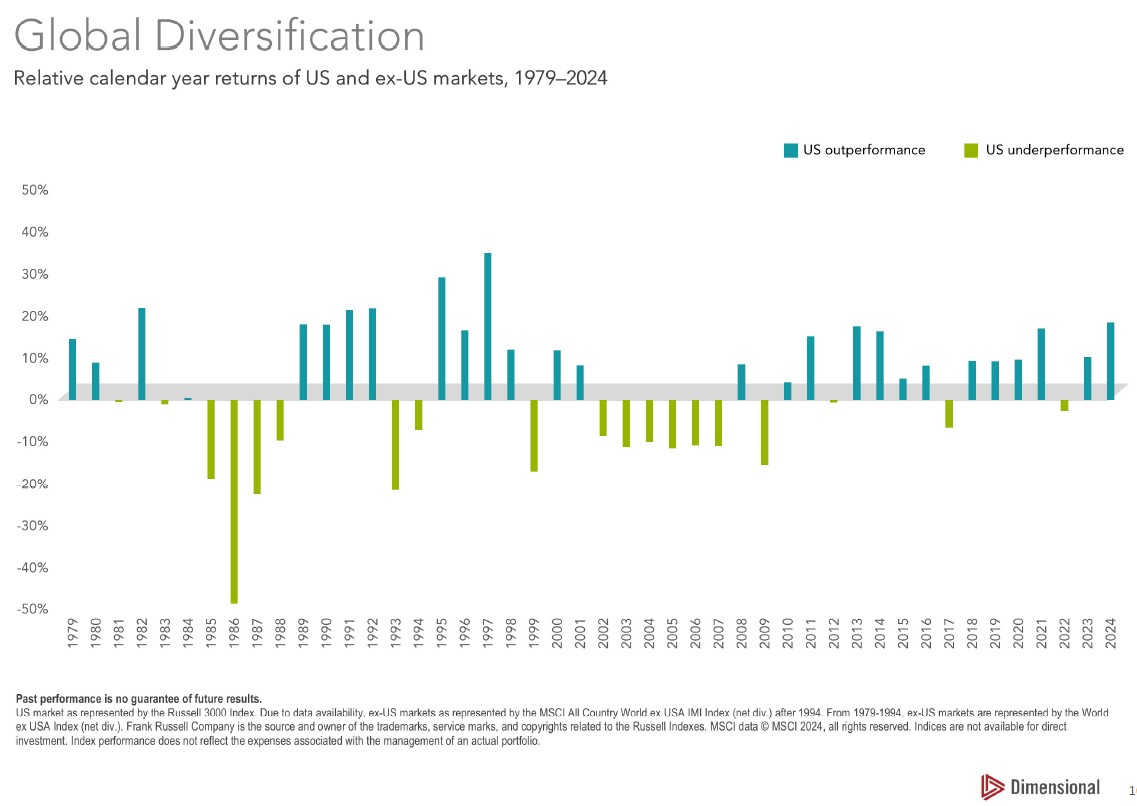

Over longer periods, leadership has moved back and forth between the U.S. and international markets.

Blue bars show years when the U.S. outperformed. Green bars show years when international markets led. The pattern is clear: leadership rotates. In retirement, the goal isn’t to win a performance contest. It’s about improving the durability of the plan.

How This Shows Up in Portfolios

In practice, investing beyond the U.S. doesn’t mean taking outsized risks, aggressive positioning or tactical bets.

For most retirement-focused portfolios, international exposure means:

- A strong U.S. equity core

- Meaningful exposure to developed international markets

- A measured allocation to emerging markets

- Ongoing rebalancing—not reactive changes

The emphasis is on structure, discipline, and consistency—not forecasts.

The Bottom Line

Evidence-based investing accepts an uncomfortable truth: we don’t know which market will win next. So instead of relying on predictions, we build portfolios designed to hold up across a wide range of outcomes.

Investing beyond the U.S. isn’t about taking more risk. It’s about managing the risks that matter most in retirement.

If you’d like to review how international exposure fits into your own plan, we’re always happy to have that conversation.